Blog Write Location: East End, Newcastle NSW 2300

Date: MAR 07 2025

So you have read about 0% finance, and providers promise it’s legit. Let’s check if it is.

When researching solar power installations, you’ve probably noticed the appealing offers of “0% interest” finance provided by Buy Now, Pay Later (BNPL) companies like Brighte. At face value, these offers seem like a dream—install solar now, pay later, and supposedly on a 0% loan with minimal costs and fees. But is this too good to be true?

Let’s shed some sunlight on what’s really going on behind these enticing promotions.

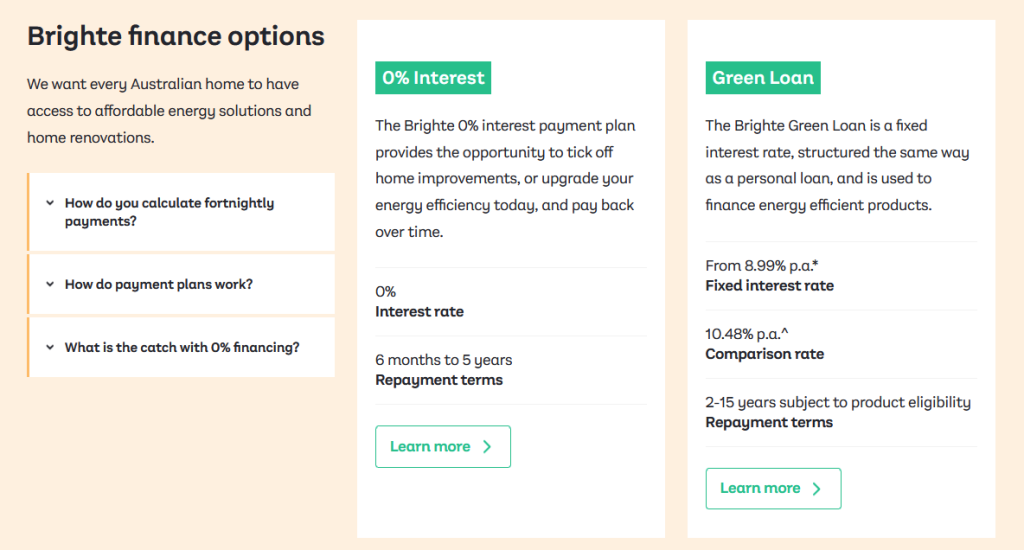

First, a picture paints 1000 words such as the one I have inserted above.

Why on earth would anyone choose a green loan over the 0% interest loan. It’s a no brainier right? 0% Interest is better than 10.48% !!

Ah yes. You have fallen forgotten the an important rule of life. Nothing in this world is free. Interest is defined as the cost of borrowing money – and you are telling me that someone is going to give you money – for 0% interest – or 0% cost? BS.

How 0% Solar Power Finance Really Works. But First…

A freely downloadable document off the internet, that describes how BNPL companies charge installers a Vendor Certainty Fee, when a loan deal is closed.

The Real Cost of “Interest-Free” Solar Financing

The “no-interest” marketing tagline used by solar finance providers such as Brighte often leads consumers to believe they’re getting free money. However, the reality is different. While you’re not charged explicit interest rates, a hidden “Vendor Certainty Fee” (VCF) is charged by BNPL providers to solar installers.

This fee, typically ranging anywhere from 5% up to around 10% of the total sale price, is paid directly by your solar installer to the finance provider. And here’s the catch: installers are contractually prohibited from directly passing this fee on to you through a surcharge or clearly labelled additional charge.

In other words, the installer absorbs a hefty financing cost from the sale price, directly impacting their bottom line.

Transparency Issues – What the “No Surcharge Rule” Means for You

Brighte, like many other BNPL providers, enforces what is known as a “no-surcharge” rule. Installers cannot directly add or itemise this financing fee on your invoice as a separate cost. The intention is good in theory—protecting consumers from surprise charges. However, in practice, it unintentionally creates a lack of transparency.

Customers think they’re getting an interest-free deal, but they’re unknowingly covering financing costs through elevated prices or lower-quality components. This hidden cost can diminish the long-term savings solar energy should provide.

How Installers Recoup These Hidden Fees

Faced with losing up to 10% of the sale price, installers must find alternative ways to recover these costs without breaking their contractual obligation to avoid explicitly passing it on as a surcharge. Here are some common methods installers may employ:

Method 1: Inflated Initial Pricing

Imagine you’re considering a 6.6kW solar system that normally costs around $10,000 installed. The installer knows that they’ll have to pay 10% ($1,000) of that amount as a finance fee to the BNPL provider.

To compensate, the installer might quietly increase their listed price from $10,000 to around $11,000.

- Normal system cost (without BNPL): $10,000

- Adjusted price (with BNPL 10% fee): $11,000

- What installer receives after paying BNPL fee: $9,900

This scenario nearly covers the installer’s fee entirely, but it’s a hidden charge to you, the consumer, cleverly embedded within the “interest-free” deal.

Method 2: Reduced Product Quality

Another indirect method some installers may use is to subtly lower their costs elsewhere, such as choosing cheaper solar panels or inverters.

While the quoted price remains at $10,000, cheaper components might be installed, saving the installer $500 to $1,000. Unfortunately, these savings come directly at the expense of quality and longevity.

Method 3: Additional Indirect Fees

Some installers introduce or increase administration fees, installation fees, or charges for supplementary services. These costs might previously have been free or significantly lower, but are now subtly higher to offset the BNPL provider’s fee.

For example, an installer might add a previously non-existent “Admin fee” of $250 or increase electrical upgrade charges to recover some costs without explicitly linking it to financing.

Is Solar Financing Always a Bad Idea?

No, solar financing itself is not inherently bad. It makes sense for many homeowners who don’t have upfront cash to invest in solar power. However, it’s crucial to distinguish between clear, transparent loans—where you’re fully aware of interest rates and repayment terms—and “interest-free” financing that conceals the true cost.

Transparent financing options might include traditional personal loans or home improvement loans with clear interest charges. While you’ll explicitly see the cost of financing, these traditional loans are often more competitively priced and easier to compare, offering more informed choices and peace of mind.

Closing Words

Look, let’s wrap it up like this. If a solar power installer is going to get charged 5-10% to sell a solar power system, as apart of this Vendor Certainty Fee, how one earth do you think these installers are going to recoup these costs?

Do you honestly expect us to believe that installers are going to take a hit to their bottom line?

OF COURSE NOT.

Be a smart consumer. Nothing in life is free. If it is 0% interest, you are paying for it – you have to pay for it – somehow. Otherwise, who will?

It is that somehow that BNPL providers are obscure on. Ask them – go on – call them – ask them how the installer will recover the costs of the VCF. Let us know what they say.

- Disclaimer: Figures such as 5-10% are not attributed to any company they are expected industry averages – they could be higher. All information we have used is derived from publicly available information.

Click the image to see what Newy Solar Co offer in terms of finance options. Straightforward, low interest, no fee loans with no exit clauses are the most transparent and straightforward loan structures we have found. And we have partnered with the best ones.